For two decades, “online payment” and “credit card” were close to synonymous. Visa and Mastercard built the rails, merchants integrated them, and consumers learned to enter sixteen-digit numbers on every checkout page. That world is fading. In 2026, the majority of e-commerce transactions in many regions no longer involve a credit or debit card at all. Customers are paying through digital wallets, instant bank transfers, vouchers, mobile money, buy-now-pay-later providers, and a long tail of region-specific payment methods that didn’t exist five years ago. Collectively, these are alternative payment methods — APMs — and the merchants who treat them as marginal options are the ones losing conversions to competitors who don’t.

This longread takes a serious look at the APM landscape: what exactly counts as an alternative payment method, why adoption has accelerated, where the regional patterns differ, and how merchants should approach the integration challenge without drowning in vendor logos.

What Counts as an APM

“Alternative payment method” is a category defined by exclusion. It refers to anything that isn’t a traditional Visa, Mastercard, or American Express card transaction. That definition is broad enough to include payment methods that share almost nothing in common with each other. A German customer using SOFORT to authorize a bank transfer, a Filipino customer topping up via GCash, and a Brazilian customer scanning a Pix QR code are all using APMs — but the technology, settlement timing, and consumer experience differ in fundamental ways.

The most useful way to organize APMs is by underlying mechanism rather than by brand. There are roughly six categories that cover the majority of global volume. Bank-based methods route money directly between accounts, either through Open Banking APIs, instant payment rails like SEPA Instant or Pix, or older direct debit schemes. Digital wallets — PayPal, Apple Pay, Google Pay, Alipay, WeChat Pay, MercadoPago — store payment credentials in a third-party account and front the transaction. Mobile money services, dominant in much of Africa, link payment authority to a phone number rather than a bank account. Vouchers and prepaid cash methods like Paysafecard and Multibanco let unbanked customers convert physical cash into online purchasing power. Buy-now-pay-later providers extend short-term credit at checkout. And cryptocurrency settlement, increasingly mainstream through stablecoins like USDT and USDC, sits at the edge of the category but is becoming a real channel for cross-border merchants.

This taxonomy matters because the operational implications cascade from it. A merchant integrating PayPal is solving a different problem from a merchant integrating Pix, even though both are technically APMs. The settlement timing, fee structure, fraud profile, and customer demographic vary dramatically. Treating them as a single category — “add APMs to checkout” — is a recipe for shallow implementations that capture none of the upside.

Why APMs Are Winning

Three forces have driven APMs from afterthought to dominant. The first is consumer preference, especially among younger demographics. Surveys consistently show that Gen Z and younger millennials prefer digital wallets and instant bank methods over manually entering card details. The reasons are practical: wallets remember credentials, biometric authentication is faster than typing, and many consumers no longer see a meaningful difference between “paying with a card” and “paying with their phone.” In markets like China, this preference is so absolute that cards have effectively been displaced — Alipay and WeChat Pay handle the overwhelming majority of consumer transactions, and merchants who only accept cards lose access to most of the market.

The second force is structural cost. Card networks charge interchange, scheme fees, processor margins, and a long tail of compliance overhead that adds up to 1.5%-3.5% per transaction in most jurisdictions. Many APMs are dramatically cheaper. Open Banking transfers in the EU often cost flat fees in cents rather than percentages. Pix in Brazil costs almost nothing for consumer-to-merchant transfers. Mobile money providers charge percentages but typically in the 0.5%-1.5% range. For merchants running thin margins or high volume, the savings translate directly into competitive advantage on pricing or marketing budget.

The third force is regulatory. The EU’s PSD2 forced banks to expose payment APIs, which created the foundation for Open Banking. India’s UPI was a top-down state initiative. Brazil’s Pix was launched and mandated by the central bank. Nigeria’s instant payment infrastructure has been driven by Central Bank policy. In each case, governments concluded that card networks extracted excessive fees from domestic commerce and built alternatives that were either free or near-free at the point of use. Merchants in these markets didn’t choose APMs voluntarily so much as they were placed in environments where APMs are the default and cards are the niche.

Specialized providers like TODA Pay have built their business around helping merchants navigate this fragmentation. Rather than integrating dozens of APMs separately — each with its own API quirks, settlement timing, and reconciliation logic — merchants connect once and gain access to the relevant methods for their target markets. The orchestration layer handles the rest.

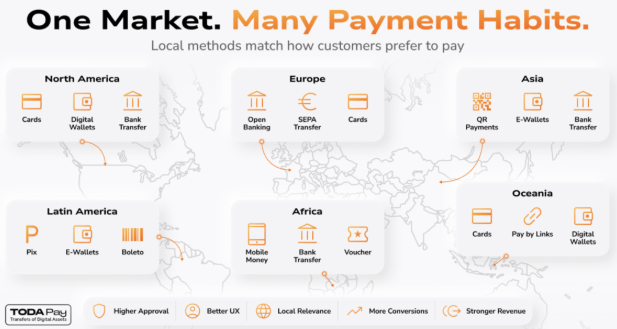

Regional Patterns That Actually Matter

APM adoption is profoundly regional. A merchant who picks payment methods based on global market share data will end up with a checkout page that converts poorly almost everywhere. The right approach is to understand which methods dominate in which regions and design accordingly.

In Western Europe, the picture is fragmented but coherent. Germany, Austria, and Switzerland lean heavily on bank transfers — SOFORT, Giropay, and direct debit schemes — combined with PayPal. The Netherlands runs almost entirely on iDEAL, which handles roughly 70% of e-commerce transactions. Belgium uses Bancontact. France is more card-friendly but increasingly accepts PayPal and Apple Pay alongside. Italy and Spain use a mix of cards, PayPal, and emerging local methods. Across the region, contactless mobile wallets are growing fast for in-person payments and bleeding into e-commerce through mobile checkout.

Northern and Eastern Europe show distinct patterns. The Nordics use Klarna, Trustly, and Swish heavily — Sweden’s domestic instant payment system. The Baltics, Czech Republic, and Hungary mix local bank transfers with cards and PayPal. Russia and the CIS region historically used local methods like Yandex.Money and QIWI, though geopolitics has reshaped this landscape significantly since 2022.

Latin America is dominated by Brazil’s Pix and Mexico’s growing instant payment systems, alongside region-specific methods like Boleto for cash payments and OXXO Pay for over-the-counter transactions. Pix has become so universal in Brazil — covering well over 80% of digital transactions — that international merchants entering the market without it are at a structural disadvantage. Argentina, Colombia, and Chile each have their own dominant local players.

Africa is the region where APMs aren’t just relevant but constitutive. Card penetration is low across much of the continent, and traditional banking infrastructure has gaps. Mobile money — M-Pesa in Kenya and Tanzania, MTN MoMo across West and Central Africa, Airtel Money in multiple markets — handles enormous transaction volumes for populations that are largely unbanked by traditional metrics. Nigeria’s instant payment infrastructure is sophisticated and growing fast. South Africa has a more developed banking sector and accepts a mix of cards, EFT transfers, and emerging APMs. Egypt, Morocco, and Ghana each have distinct payment ecosystems. For merchants targeting African consumers, the question isn’t “should we add APMs” but “which APMs cover which countries with what coverage and cost.”

Asia is the most diverse region of all. China is essentially a closed Alipay/WeChat Pay ecosystem. Japan uses cards heavily but adoption of LINE Pay and PayPay is growing. South Korea has KakaoPay and Naver Pay. Southeast Asia — Indonesia, Thailand, Vietnam, Philippines — runs on a mix of GrabPay, OVO, GoPay, GCash, and other regional wallets, with QR-based payments dominant. India’s UPI is one of the largest payment systems in the world by transaction count and is required for any merchant operating in the country.

The Integration Problem

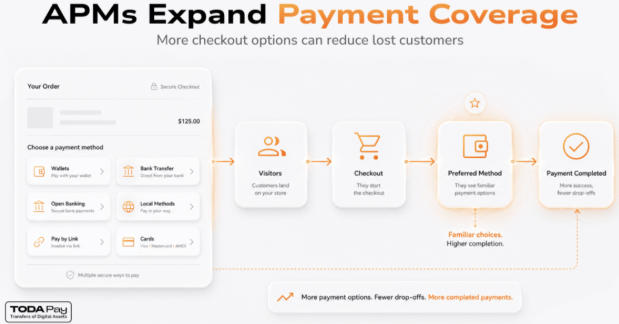

Reading the regional breakdown, the obvious challenge becomes clear. A merchant operating across Europe, Latin America, and parts of Africa might need to support thirty or forty different payment methods to cover the dominant options in each market. Each method has its own API, its own settlement rhythm, its own fee structure, its own fraud rules, and its own reconciliation requirements.

There are, broadly, three approaches to this problem. The first is direct integration — connecting to each APM provider individually. This produces the deepest control and often the best fees per method, but the engineering and operational overhead is enormous. Each new market requires a new integration project, ongoing maintenance, and a separate reconciliation workflow. For most merchants, this is only realistic if they have a dedicated payments engineering team and high enough volume to justify the investment.

The second approach is acquirer-led. The merchant signs with a major acquirer (a Worldpay, Adyen, Stripe, or similar) and uses that provider’s APM coverage. This is faster to implement but typically delivers shallower regional depth. Major global acquirers cover the obvious APMs — PayPal, Apple Pay, Google Pay, the largest European bank methods — but coverage in emerging markets and niche local methods is often weak or absent. Merchants who try to scale into Africa or Latin America with a primarily-card-network acquirer often discover that the supposed “APM coverage” is missing exactly the methods that matter for those markets.

The third approach is specialized payment providers focused on APMs and emerging markets. These providers integrate dozens or hundreds of local methods, normalize the API surface, and handle the orchestration logic. They typically don’t try to compete with the global card acquirers on card processing — instead, they complement them, sitting alongside in a multi-provider architecture. Smart routing decides which provider handles which transaction in real time based on which method the customer chooses, what’s online, and what produces the best approval rate.

This is the model that providers like TODA Pay have built around. By combining alternative payment method coverage with payment orchestration, they let merchants treat APMs as a single capability rather than a sprawl of separate integrations. The orchestration layer also handles fallback logic — if a primary method is unavailable, the customer is routed to an alternative without abandoning checkout.

Practical Selection Criteria

Merchants evaluating APM coverage should focus on questions that surface real differences between providers, not marketing claims.

- Which specific methods are supported in your top three target markets, and at what depth? “Africa coverage” is meaningless without country and method breakdown.

- Are connections direct or routed through aggregators? Direct connections are faster and more reliable; aggregator-routed methods can fail in ways that are hard to diagnose.

- What is the settlement timing for each method? Some APMs settle instantly, others take days. Cash flow planning depends on knowing this per-method, not in aggregate.

- How is fraud handled? Different APMs have radically different fraud profiles. Mobile money has unique fraud patterns. Vouchers carry different risks. The provider should have method-specific fraud logic, not just a generic card-fraud engine applied universally.

- What does reconciliation look like? Multi-method, multi-currency, multi-region operations create reconciliation complexity that can swamp finance teams. Providers that deliver clean unified reporting across methods are worth a premium.

- How are new methods added? Markets evolve. New APMs launch. The provider should have a track record of adding new methods quickly when they reach commercial scale.

The 2026 Trajectory

Three trends will shape APMs through the rest of the year and into 2027. First, instant payment rails will keep proliferating. Pix, UPI, FedNow in the US, Brazil’s PIX expansion to international corridors — the global pattern is unambiguous. Within five years, near-instant settlement on domestic rails will be the default expectation in essentially every developed market.

Second, mobile wallets will continue consolidating power, but the pattern will differ by region. Apple Pay and Google Pay dominate developed-market checkouts as a UX layer over cards and bank methods. In Asia and parts of Africa, super-app wallets that combine payment with messaging, commerce, and financial services will keep extending their reach. The implication for merchants: “adding a wallet button” is not a strategy. Understanding which wallet’s user base maps to which customer segment is.

Third, the line between APM and infrastructure will continue to blur. Stablecoin settlement, embedded finance, and the growing capability of payment orchestration platforms mean that the APM layer is increasingly part of broader merchant operations rather than a standalone checkout decision. Picking a provider in 2026 is less about “which payment buttons do you offer” and more about “what does your platform let us build”.

Conclusion

Alternative payment methods aren’t alternative anymore. In most regions and most demographics, they are the primary way customers want to pay online. The merchants capturing the upside are the ones who treat APMs as a strategic capability — picking providers with depth in their target markets, integrating intelligently rather than exhaustively, and using orchestration to make the complexity invisible to the end customer.

The risk for merchants who treat APMs as an afterthought is structural. Conversion drops in markets where dominant methods aren’t supported. Fees stay higher than they need to be. Approval rates trail competitors. Cross-border expansion stalls because the payment layer can’t keep up. None of this shows up as a single dramatic failure — it shows up as a slow accumulation of underperformance that’s invisible in the dashboard but visible in the financials. Treating APMs seriously, working with the right specialized partners, and building checkout experiences that reflect regional reality is what separates the merchants who scale from the ones who plateau.